Should there be demand-based recurring fees on ENS domains?

2022 Sep 09

See all posts

Should there be demand-based recurring fees on ENS domains?

Special thanks to Lars Doucet, Glen Weyl and Nick Johnson for

discussion and feedback on various topics.

ENS domains today are cheap. Very cheap. The cost to register and

maintain a five-letter domain name is only $5

per year. This sounds reasonable from the perspective of one person

trying to register a single domain, but it looks very different when you

look at the situation globally: when ENS was younger, someone could have

registered all 8938 five-letter words in the Scrabble

wordlist (which includes exotic stuff like "BURRS", "FLUYT" and

"ZORIL") and pre-paid their ownership for a hundred years, all for the

price of a

dozen lambos. And in fact, many people did: today, almost all of

those five-letter words are already taken, many by squatters waiting for

someone to buy the domain from them at a much higher price. A random

scrape of OpenSea shows that about 40% of all these domains are for sale

or have been sold on that platform alone.

The question worth asking is: is this really the best way to allocate

domains? By selling off these domains so cheaply, ENS DAO is almost

certainly gathering far less revenue than it could, which limits its

ability to act to improve the ecosystem. The status quo is also bad for

fairness: being able to buy up all the domains cheaply was great for

people in 2017, is okay in 2022, but the consequences may severely

handicap the system in 2050. And given that buying a five-letter-word

domain in practice costs anywhere from 0.1 to 500

ETH, the notionally cheap registration prices are not actually

providing cost savings to users. In fact, there are deep

economic reasons

to believe that reliance on secondary markets makes domains

more expensive than a well-designed in-protocol mechanism.

Could we allocate ongoing ownership of domains in a better way? Is

there a way to raise more revenue for ENS DAO, do a better job

of ensuring domains go to those who can make best use of them, and at

the same time preserve the credible neutrality and the accessible very

strong guarantees of long-term ownership that make ENS valuable?

Problem

1: there is a fundamental tradeoff between strength of property rights

and fairness

Suppose that there are \(N\)

"high-value names" (eg. five-letter words in the Scrabble dictionary,

but could be any similar category). Suppose that each year, users grab

up \(k\) names, and some portion \(p\) of them get grabbed by someone who's

irrationally stubborn and not willing to give them up (\(p\) could be really low, it just needs to

be greater than zero). Then, after \(\frac{N}{k * p}\) years, no one will be

able to get a high-value name again.

This is a two-line mathematical theorem, and it feels too simple to

be saying anything important. But it actually gets at a crucial truth:

time-unlimited allocation of a finite resource is incompatible with

fairness across long time horizons. This is true for land; it's the

reason why there have been so

many land reforms throughout history, and it's a big part of why

many advocate for land taxes

today. It's also true for domains, though the problem in the

traditional domain space has been temporarily alleviated by a "forced

dilution" of early .com holders in the form of a mass introduction of

.io, .me, .network and many other domains. ENS has

soft-committed to not add new TLDs to avoid polluting the global

namespace and rupturing its chances of eventual integration with

mainstream DNS, so such a dilution is not an option.

Fortunately, ENS charges not just a one-time fee to register a

domain, but also a recurring annual fee to maintain it. Not all

decentralized domain name systems had the foresight to implement this;

Unstoppable Domains did not, and even goes so far as to proudly

advertise its preference for short-term consumer appeal over long-term

sustainability ("No renewal

fees ever!"). The recurring fees in ENS and traditional DNS are a

healthy mitigation to the worst excesses of a truly unlimited

pay-once-own-forever model: at the very least, the recurring fees mean

that no one will be able to accidentally lock down a domain forever

through forgetfulness or carelessness. But it may not be enough. It's

still possible to spend $500 to lock down an ENS domain for an entire

century, and there are certainly some types of domains that are in high

enough demand that this is vastly underpriced.

Problem

2: speculators do not actually create efficient markets

Once we admit that a first-come-first-serve model with low fixed fees

has these problems, a common counterargument is to say: yes, many of the

names will get bought up by speculators, but speculation is natural and

good. It is a free market mechanism, where speculators who actually want

to maximize their profit are motivated to resell the domain in such a

way that it goes to whoever can make the best use of the domain, and

their outsized returns are just compensation for this service.

But as it turns out, there has been academic research on this topic,

and it is not actually true that profit-maximizing auctioneers maximize

social welfare! Quoting Myerson

1981:

By announcing a reservation price of 50, the seller risks a

probability \((1 / 2^n)\) of keeping

the object even though some bidder is willing to pay more than \(t_0\) for it; but the seller also increases

his expected revenue, because he can command a higher price when the

object is sold.

Thus the optimal auction may not be ex-post efficient. To see more

clearly why this can happen, consider the example in the above

paragraph, for the case when \(n = 1\)

... Ex post efficiency would require that the bidder must always get the

object, as long as his value estimate is positive. But then the bidder

would never admit to more than an infinitesimal value estimate, since

any positive bid would win the object ... In fact the seller's optimal

policy is to refuse to sell the object for less than 50.

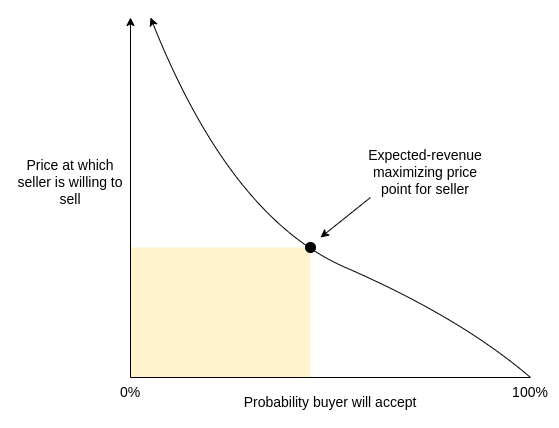

Translated into diagram form:

Maximizing revenue for the seller almost always requires accepting

some probability of never selling the domain at all, leaving it unused

outright. One important nuance in the argument is that

seller-revenue-maximizing auctions are at their most inefficient when

there is one possible buyer (or at least, one buyer with a valuation far

above the others), and the inefficiency decreases quickly once there are

many competing potential buyers. But for a large class of domains, the

first category is precisely the situation they are in. Domains that are

simply some person, project or company's name, for example, have one

natural buyer: that person or project. And so if a speculator buys up

such a name, they will of course set the price high, accepting a large

chance of never coming to a deal to maximize their revenue in the case

where a deal does arise.

Hence, we cannot say that speculators grabbing a large portion of

domain allocation revenues is merely just compensation for them ensuring

that the market is efficient. On the contrary, speculators can easily

make the market worse than a well-designed mechanism in the

protocol that encourages domains to be directly available for sale at

fair prices.

One

cheer for stricter property rights: stability of domain ownership has

positive externalities

The monopoly problems of overly-strict property rights on

non-fungible assets have been known for a long time. Resolving this

issue in a market-based way was the original goal of Harberger

taxes: require the owner of each covered asset to set a price at

which they are willing to sell it to anyone else, and charge an annual

fee based on that price. For example, one could charge 0.5% of the sale

price every year. Holders would be incentivized to leave the asset

available for purchase at prices that are reasonable, "lazy" holders who

refuse to sell would lose money every year, and hoarding assets without

using them would in many cases become economically infeasible

outright.

But the risk of being forced to sell something at any time can have

large economic and psychological costs, and it's for this reason that

advocates of Harberger taxes generally focus on industrial property

applications where the market participants are sophisticated. Where do

domains fall on the spectrum? Let us consider the costs of a business

getting "relocated", in three separate cases: a data center, a

restaurant, and an ENS name.

|

Data center |

Restaurant |

ENS name |

| Confusion from people expecting old location |

An employee comes to the old location, and unexpectedly finds it

closed. |

An employee or a customer comes to the old location, and

unexpectedly finds it closed. |

Someone sends a big chunk of money to the wrong address. |

| Loss of location-specific long-term investment |

Low |

The restaurant will probably lose many long-term customers for whom

the new location is too far away |

The owner spent years building a brand around the old name that

cannot easily carry over. |

As it turns out, domains do not hold up very well. Domain name owners

are often not sophisticated, the costs of switching domain names are

often high, and negative externalities of a name-change gone wrong can

be large. The highest-value owner of coinbase.eth may not

be Coinbase; it could just as easily be a scammer who would grab up the

domain and then immediately make a fake charity or ICO claiming it's run

by Coinbase and ask people to send that address their money. For

these reasons, Harberger taxing domains is not a great

idea.

Alternative

solution 1: demand-based recurring pricing

Maintaining ownership over an ENS domain today requires paying a

recurring fee. For most domains, this is a simple and very low $5 per

year. The only exceptions are four-letter domains ($160 per year) and

three-letter domains ($640 per year). But what if instead, we make the

fee somehow depend on the actual level of market demand for the

domain?

This would not be a Harberger-like scheme where you have to make the

domain available for immediate sale at a particular price.

Rather, the initiative in the price-setting procedure would fall on the

bidders. Anyone could bid on a particular domain, and if they keep an

open bid for a sufficiently long period of time (eg. 4 weeks), the

domain's valuation rises to that level. The annual fee on the domain

would be proportional to the valuation (eg. it might be set to 0.5% of

the valuation). If there are no bids, the fee might decay at a constant

rate.

When a bidder sends their bid amount into a smart contract to place a

bid, the owner has two options: they could either accept the bid, or

they could reject, though they may have to start paying a higher price.

If a bidder bids a value higher than the actual value of the domain, the

owner could sell to them, costing the bidder a huge amount of money.

This property is important, because it means that "griefing"

domain holders is risky and expensive, and may even end up benefiting

the victim. If you own a domain, and a powerful actor wants to

harass or censor you, they could try to make a very high bid for that

domain to greatly increase your annual fee. But if they do this, you

could simply sell to them and collect the massive payout.

This already provides much more stability and is more noob-friendly

than a Harberger tax. Domain owners don't need to constantly worry

whether or not they're setting prices too low. Rather, they can simply

sit back and pay the annual fee, and if someone offers to bid they can

take 4 weeks to make a decision and either sell the domain or continue

holding it and accept the higher fee. But even this probably does not

provide quite enough stability. To go even further, we need a compromise

on the compromise.

Alternative

solution 2: capped demand-based recurring pricing

We can modify the above scheme to offer even stronger guarantees to

domain-name holders. Specifically, we can try to offer the following

property:

Strong time-bound ownership guarantee: for any fixed

number of years, it's always possible to compute a fixed amount of money

that you can pre-pay to unconditionally guarantee ownership for at

least that number of years.

In math language, there must be some function \(y = f(n)\) such that if you pay \(y\) dollars (or ETH), you get a hard

guarantee that you will be able to hold on to the domain for at least

\(n\) years, no matter what happens.

\(f\) may also depend on other

factors, such as what happened to the domain previously, as long as

those factors are known at the time the transaction to register or

extend a domain is made. Note that the maximum annual fee after

\(n\) years would be the derivative

\(f'(n)\).

The new price after a bid would be capped at the implied maximum

annual fee. For example, if \(f(n) =

\frac{1}{2}n^2\), so \(f'(n) =

n\), and you get a bid of $5 after 7 years, the annual fee would

rise to $5, but if you get a bid of $10 after 7 years, the annual fee

would only rise to $7. If no bids that raise the fee to the max are made

for some length of time (eg. a full year), \(n\) resets. If a bid is made and rejected,

\(n\) resets.

And of course, we have a highly subjective criterion that \(f(n)\) must be "reasonable". We can create

compromise proposals by trying different shapes for \(f\):

| Type |

\(f(n)\) (\(p_0\) = price of last sale or last rejected

bid, or $1 if most recent event is a reset) |

In plain English |

Total cost to guarantee holding for >= 10 years |

Total cost to guarantee holding for >= 100 years |

| Exponential fee growth |

\(f(n) = \int_0^n p_0 *

1.1^n\) |

The fee can grow by a maximum of 10% per year (with

compounding). |

$836 |

$7.22m |

| Linear fee growth |

\(f(n) = p_0 * n +

\frac{15}{2}n^2\) |

The annual fee can grow by a maximum of $15 per year. |

$1250 |

$80k |

| Capped annual fee |

\(f(n) = 640 * n\) |

The annual fee cannot exceed $640 per year. That is, a domain in

high demand can start to cost as much as a three-letter domain, but not

more. |

$6400 |

$64k |

Or in chart form:

Note that the amounts in the table are only the theoretical

maximums needed to guarantee holding a domain for that number of

years. In practice, almost no domains would have bidders willing to bid

very high amounts, and so holders of almost all domains would end up

paying much less than the maximum.

One fascinating property of the "capped annual fee" approach

is that there are versions of it that are strictly more

favorable to existing domain-name holders than the status

quo. In particular, we could imagine a system where a domain

that gets no bids does not have to pay any annual fee, and a

bid could increase the annual fee to a maximum of $5 per year.

Demand from external bids clearly provides some signal about

how valuable a domain is (and therefore, to what extent an owner is

excluding others by maintaining control over it). Hence,

regardless of your views on what level of fees should be

required to maintain a domain, I would argue that you should find

some parameter choice for demand-based fees

appealing.

I will still make my case for why some superlinear \(f(n)\), a max annual fee that goes up over

time, is a good idea. First, paying more for longer-term security is a

common feature throughout the economy. Fixed-rate mortgages usually have

higher

interest rates than variable-rate mortgages. You can get

higher interest by providing deposits that are locked up for longer

periods of time; this is compensation the bank pays you for

providing longer-term security to the bank. Similarly,

longer-term government bonds typically have higher yields.

Second, the annual fee should be able to eventually adjust to

whatever the market value of the domain is; we just don't want that to

happen too quickly.

Superlinear \(f(n)\) values still

make hard guarantees of ownership reasonably accessible over pretty long

timescales: with the linear-fee-growth formula \(f(n) = p_0 * n + \frac{15}{2}n^2\), for

only $6000 ($120 per year) you could ensure ownership of the domain for

25 years, and you would almost certainly pay much less. The ideal of

"register and forget" for censorship-resistant services would still be

very much available.

From here to there

Weakening property norms, and increasing fees, is psychologically

very unappealing to many people. This is true even when these fees make

clear economic sense, and even when you can redirect fee revenue into a

UBI and mathematically show that the majority of people would

economically net-benefit from your proposal. Cities have a hard time adding

congestion pricing, even when it's painfully clear that the only two

choices are paying congestion fees in dollars and paying congestion fees

in wasted time and

weakened mental health driving in painfully slow traffic. Land value taxes, despite being in

many ways one

of the most effective and least harmful taxes out there, have a hard

time getting adopted. Unstoppable Domains's loud and proud advertisement

of "no renewal fees ever" is in my view very short-sighted, but it's

clearly at least somewhat effective. So how could I possibly

think that we have any chance of adding fees and conditions to domain

name ownership?

The crypto space is not going to solve deep challenges in human

political psychology that humanity has failed at for centuries. But we

do not have to. I see two possible answers that do have some

realistic hope for success:

Democratic legitimacy: come up with a compromise proposal

that really is a sufficient compromise that it makes enough people

happy, and perhaps even makes some existing domain name holders

(not just potential domain name holders) better off

than they are today.

For example, we could implement demand-based annual fees (eg. setting

the annual fee to 0.5% of the highest bid) with a fee cap of $640 per

year for domains up to eight letters long, and $5 per year for longer

domains, and let domain holders pay nothing if no one makes a bid. Many

average users would save money under such a proposal.

Market legitimacy: avoid the need to get legitimacy to

overturn people's expectations in the existing system by instead

creating a new system (or sub-system).

In traditional DNS, this could be done just by creating a new TLD

that would be as convenient as existing TLDs. In ENS, there is a stated

desire to stick to .eth only to avoid conflicting with the

existing domain name system. And using existing subdomains doesn't quite

work: foo.bar.eth is much less nice than

foo.eth. One possible middle route is for the ENS DAO to

hand off single-letter domain names solely to projects that run

some other kind of credibly-neutral marketplace for their subdomains, as

long as they hand over at least 50% of the revenue to the ENS DAO.

For example, perhaps x.eth could use one of my proposed

pricing schemes for its subdomains, and t.eth could

implement a mechanism where ENS DAO has the right to forcibly transfer

subdomains for anti-fraud and trademark reasons. foo.x.eth

just barely looks good enough to be sort-of a substitute for

foo.eth; it will have to do.

If making changes to ENS domain pricing itself are off the table,

then the market-based approach of explicitly encouraging marketplaces

with different rules in subdomains should be strongly considered.

To me, the crypto space is not just about coins, and I admit my

attraction to ENS does not center around some notion of

unconditional and infinitely strict property-like ownership

over domains. Rather, my interest in the space lies more in credible

neutrality, and property rights that are strongly protected

particularly against politically motivated censorship and arbitrary and

targeted interference by powerful actors. That said, a high degree of

guarantee of ownership is nevertheless very important for a domain name

system to be able to function.

The hybrid proposals I suggest above are my attempt at preserving

total credible neutrality, continuing to provide a high degree of

ownership guarantee, but at the same time increasing the cost of domain

squatting, raising more revenue for the ENS DAO to be able to work on

important public goods, and improving the chances that people

who do not have the domain they want already will be able to get

one.

Should there be demand-based recurring fees on ENS domains?

2022 Sep 09 See all postsSpecial thanks to Lars Doucet, Glen Weyl and Nick Johnson for discussion and feedback on various topics.

ENS domains today are cheap. Very cheap. The cost to register and maintain a five-letter domain name is only $5 per year. This sounds reasonable from the perspective of one person trying to register a single domain, but it looks very different when you look at the situation globally: when ENS was younger, someone could have registered all 8938 five-letter words in the Scrabble wordlist (which includes exotic stuff like "BURRS", "FLUYT" and "ZORIL") and pre-paid their ownership for a hundred years, all for the price of a dozen lambos. And in fact, many people did: today, almost all of those five-letter words are already taken, many by squatters waiting for someone to buy the domain from them at a much higher price. A random scrape of OpenSea shows that about 40% of all these domains are for sale or have been sold on that platform alone.

The question worth asking is: is this really the best way to allocate domains? By selling off these domains so cheaply, ENS DAO is almost certainly gathering far less revenue than it could, which limits its ability to act to improve the ecosystem. The status quo is also bad for fairness: being able to buy up all the domains cheaply was great for people in 2017, is okay in 2022, but the consequences may severely handicap the system in 2050. And given that buying a five-letter-word domain in practice costs anywhere from 0.1 to 500 ETH, the notionally cheap registration prices are not actually providing cost savings to users. In fact, there are deep economic reasons to believe that reliance on secondary markets makes domains more expensive than a well-designed in-protocol mechanism.

Could we allocate ongoing ownership of domains in a better way? Is there a way to raise more revenue for ENS DAO, do a better job of ensuring domains go to those who can make best use of them, and at the same time preserve the credible neutrality and the accessible very strong guarantees of long-term ownership that make ENS valuable?

Problem 1: there is a fundamental tradeoff between strength of property rights and fairness

Suppose that there are \(N\) "high-value names" (eg. five-letter words in the Scrabble dictionary, but could be any similar category). Suppose that each year, users grab up \(k\) names, and some portion \(p\) of them get grabbed by someone who's irrationally stubborn and not willing to give them up (\(p\) could be really low, it just needs to be greater than zero). Then, after \(\frac{N}{k * p}\) years, no one will be able to get a high-value name again.

This is a two-line mathematical theorem, and it feels too simple to be saying anything important. But it actually gets at a crucial truth: time-unlimited allocation of a finite resource is incompatible with fairness across long time horizons. This is true for land; it's the reason why there have been so many land reforms throughout history, and it's a big part of why many advocate for land taxes today. It's also true for domains, though the problem in the traditional domain space has been temporarily alleviated by a "forced dilution" of early .com holders in the form of a mass introduction of .io, .me, .network and many other domains. ENS has soft-committed to not add new TLDs to avoid polluting the global namespace and rupturing its chances of eventual integration with mainstream DNS, so such a dilution is not an option.

Fortunately, ENS charges not just a one-time fee to register a domain, but also a recurring annual fee to maintain it. Not all decentralized domain name systems had the foresight to implement this; Unstoppable Domains did not, and even goes so far as to proudly advertise its preference for short-term consumer appeal over long-term sustainability ("No renewal fees ever!"). The recurring fees in ENS and traditional DNS are a healthy mitigation to the worst excesses of a truly unlimited pay-once-own-forever model: at the very least, the recurring fees mean that no one will be able to accidentally lock down a domain forever through forgetfulness or carelessness. But it may not be enough. It's still possible to spend $500 to lock down an ENS domain for an entire century, and there are certainly some types of domains that are in high enough demand that this is vastly underpriced.

Problem 2: speculators do not actually create efficient markets

Once we admit that a first-come-first-serve model with low fixed fees has these problems, a common counterargument is to say: yes, many of the names will get bought up by speculators, but speculation is natural and good. It is a free market mechanism, where speculators who actually want to maximize their profit are motivated to resell the domain in such a way that it goes to whoever can make the best use of the domain, and their outsized returns are just compensation for this service.

But as it turns out, there has been academic research on this topic, and it is not actually true that profit-maximizing auctioneers maximize social welfare! Quoting Myerson 1981:

Translated into diagram form:

Maximizing revenue for the seller almost always requires accepting some probability of never selling the domain at all, leaving it unused outright. One important nuance in the argument is that seller-revenue-maximizing auctions are at their most inefficient when there is one possible buyer (or at least, one buyer with a valuation far above the others), and the inefficiency decreases quickly once there are many competing potential buyers. But for a large class of domains, the first category is precisely the situation they are in. Domains that are simply some person, project or company's name, for example, have one natural buyer: that person or project. And so if a speculator buys up such a name, they will of course set the price high, accepting a large chance of never coming to a deal to maximize their revenue in the case where a deal does arise.

Hence, we cannot say that speculators grabbing a large portion of domain allocation revenues is merely just compensation for them ensuring that the market is efficient. On the contrary, speculators can easily make the market worse than a well-designed mechanism in the protocol that encourages domains to be directly available for sale at fair prices.

One cheer for stricter property rights: stability of domain ownership has positive externalities

The monopoly problems of overly-strict property rights on non-fungible assets have been known for a long time. Resolving this issue in a market-based way was the original goal of Harberger taxes: require the owner of each covered asset to set a price at which they are willing to sell it to anyone else, and charge an annual fee based on that price. For example, one could charge 0.5% of the sale price every year. Holders would be incentivized to leave the asset available for purchase at prices that are reasonable, "lazy" holders who refuse to sell would lose money every year, and hoarding assets without using them would in many cases become economically infeasible outright.

But the risk of being forced to sell something at any time can have large economic and psychological costs, and it's for this reason that advocates of Harberger taxes generally focus on industrial property applications where the market participants are sophisticated. Where do domains fall on the spectrum? Let us consider the costs of a business getting "relocated", in three separate cases: a data center, a restaurant, and an ENS name.

As it turns out, domains do not hold up very well. Domain name owners are often not sophisticated, the costs of switching domain names are often high, and negative externalities of a name-change gone wrong can be large. The highest-value owner of

coinbase.ethmay not be Coinbase; it could just as easily be a scammer who would grab up the domain and then immediately make a fake charity or ICO claiming it's run by Coinbase and ask people to send that address their money. For these reasons, Harberger taxing domains is not a great idea.Alternative solution 1: demand-based recurring pricing

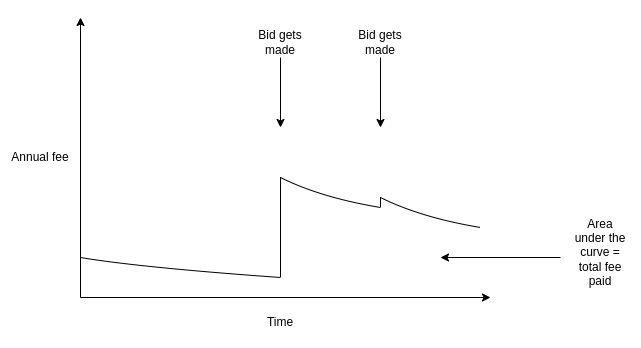

Maintaining ownership over an ENS domain today requires paying a recurring fee. For most domains, this is a simple and very low $5 per year. The only exceptions are four-letter domains ($160 per year) and three-letter domains ($640 per year). But what if instead, we make the fee somehow depend on the actual level of market demand for the domain?

This would not be a Harberger-like scheme where you have to make the domain available for immediate sale at a particular price. Rather, the initiative in the price-setting procedure would fall on the bidders. Anyone could bid on a particular domain, and if they keep an open bid for a sufficiently long period of time (eg. 4 weeks), the domain's valuation rises to that level. The annual fee on the domain would be proportional to the valuation (eg. it might be set to 0.5% of the valuation). If there are no bids, the fee might decay at a constant rate.

When a bidder sends their bid amount into a smart contract to place a bid, the owner has two options: they could either accept the bid, or they could reject, though they may have to start paying a higher price. If a bidder bids a value higher than the actual value of the domain, the owner could sell to them, costing the bidder a huge amount of money.

This property is important, because it means that "griefing" domain holders is risky and expensive, and may even end up benefiting the victim. If you own a domain, and a powerful actor wants to harass or censor you, they could try to make a very high bid for that domain to greatly increase your annual fee. But if they do this, you could simply sell to them and collect the massive payout.

This already provides much more stability and is more noob-friendly than a Harberger tax. Domain owners don't need to constantly worry whether or not they're setting prices too low. Rather, they can simply sit back and pay the annual fee, and if someone offers to bid they can take 4 weeks to make a decision and either sell the domain or continue holding it and accept the higher fee. But even this probably does not provide quite enough stability. To go even further, we need a compromise on the compromise.

Alternative solution 2: capped demand-based recurring pricing

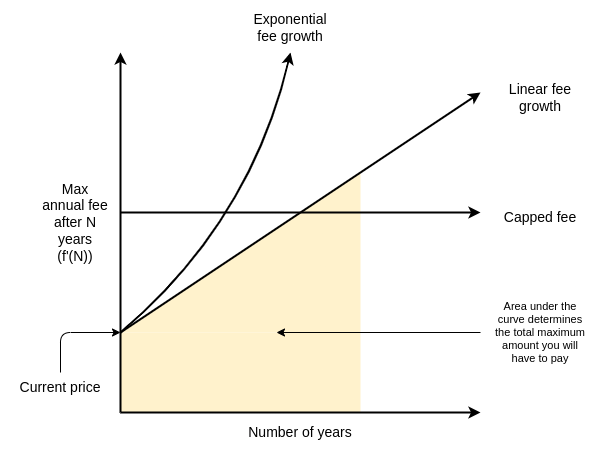

We can modify the above scheme to offer even stronger guarantees to domain-name holders. Specifically, we can try to offer the following property:

In math language, there must be some function \(y = f(n)\) such that if you pay \(y\) dollars (or ETH), you get a hard guarantee that you will be able to hold on to the domain for at least \(n\) years, no matter what happens. \(f\) may also depend on other factors, such as what happened to the domain previously, as long as those factors are known at the time the transaction to register or extend a domain is made. Note that the maximum annual fee after \(n\) years would be the derivative \(f'(n)\).

The new price after a bid would be capped at the implied maximum annual fee. For example, if \(f(n) = \frac{1}{2}n^2\), so \(f'(n) = n\), and you get a bid of $5 after 7 years, the annual fee would rise to $5, but if you get a bid of $10 after 7 years, the annual fee would only rise to $7. If no bids that raise the fee to the max are made for some length of time (eg. a full year), \(n\) resets. If a bid is made and rejected, \(n\) resets.

And of course, we have a highly subjective criterion that \(f(n)\) must be "reasonable". We can create compromise proposals by trying different shapes for \(f\):

Or in chart form:

Note that the amounts in the table are only the theoretical maximums needed to guarantee holding a domain for that number of years. In practice, almost no domains would have bidders willing to bid very high amounts, and so holders of almost all domains would end up paying much less than the maximum.

One fascinating property of the "capped annual fee" approach is that there are versions of it that are strictly more favorable to existing domain-name holders than the status quo. In particular, we could imagine a system where a domain that gets no bids does not have to pay any annual fee, and a bid could increase the annual fee to a maximum of $5 per year.

Demand from external bids clearly provides some signal about how valuable a domain is (and therefore, to what extent an owner is excluding others by maintaining control over it). Hence, regardless of your views on what level of fees should be required to maintain a domain, I would argue that you should find some parameter choice for demand-based fees appealing.

I will still make my case for why some superlinear \(f(n)\), a max annual fee that goes up over time, is a good idea. First, paying more for longer-term security is a common feature throughout the economy. Fixed-rate mortgages usually have higher interest rates than variable-rate mortgages. You can get higher interest by providing deposits that are locked up for longer periods of time; this is compensation the bank pays you for providing longer-term security to the bank. Similarly, longer-term government bonds typically have higher yields. Second, the annual fee should be able to eventually adjust to whatever the market value of the domain is; we just don't want that to happen too quickly.

Superlinear \(f(n)\) values still make hard guarantees of ownership reasonably accessible over pretty long timescales: with the linear-fee-growth formula \(f(n) = p_0 * n + \frac{15}{2}n^2\), for only $6000 ($120 per year) you could ensure ownership of the domain for 25 years, and you would almost certainly pay much less. The ideal of "register and forget" for censorship-resistant services would still be very much available.

From here to there

Weakening property norms, and increasing fees, is psychologically very unappealing to many people. This is true even when these fees make clear economic sense, and even when you can redirect fee revenue into a UBI and mathematically show that the majority of people would economically net-benefit from your proposal. Cities have a hard time adding congestion pricing, even when it's painfully clear that the only two choices are paying congestion fees in dollars and paying congestion fees in wasted time and weakened mental health driving in painfully slow traffic. Land value taxes, despite being in many ways one of the most effective and least harmful taxes out there, have a hard time getting adopted. Unstoppable Domains's loud and proud advertisement of "no renewal fees ever" is in my view very short-sighted, but it's clearly at least somewhat effective. So how could I possibly think that we have any chance of adding fees and conditions to domain name ownership?

The crypto space is not going to solve deep challenges in human political psychology that humanity has failed at for centuries. But we do not have to. I see two possible answers that do have some realistic hope for success:

Democratic legitimacy: come up with a compromise proposal that really is a sufficient compromise that it makes enough people happy, and perhaps even makes some existing domain name holders (not just potential domain name holders) better off than they are today.

For example, we could implement demand-based annual fees (eg. setting the annual fee to 0.5% of the highest bid) with a fee cap of $640 per year for domains up to eight letters long, and $5 per year for longer domains, and let domain holders pay nothing if no one makes a bid. Many average users would save money under such a proposal.

Market legitimacy: avoid the need to get legitimacy to overturn people's expectations in the existing system by instead creating a new system (or sub-system).

In traditional DNS, this could be done just by creating a new TLD that would be as convenient as existing TLDs. In ENS, there is a stated desire to stick to

.ethonly to avoid conflicting with the existing domain name system. And using existing subdomains doesn't quite work:foo.bar.ethis much less nice thanfoo.eth. One possible middle route is for the ENS DAO to hand off single-letter domain names solely to projects that run some other kind of credibly-neutral marketplace for their subdomains, as long as they hand over at least 50% of the revenue to the ENS DAO.For example, perhaps

x.ethcould use one of my proposed pricing schemes for its subdomains, andt.ethcould implement a mechanism where ENS DAO has the right to forcibly transfer subdomains for anti-fraud and trademark reasons.foo.x.ethjust barely looks good enough to be sort-of a substitute forfoo.eth; it will have to do.If making changes to ENS domain pricing itself are off the table, then the market-based approach of explicitly encouraging marketplaces with different rules in subdomains should be strongly considered.

To me, the crypto space is not just about coins, and I admit my attraction to ENS does not center around some notion of unconditional and infinitely strict property-like ownership over domains. Rather, my interest in the space lies more in credible neutrality, and property rights that are strongly protected particularly against politically motivated censorship and arbitrary and targeted interference by powerful actors. That said, a high degree of guarantee of ownership is nevertheless very important for a domain name system to be able to function.

The hybrid proposals I suggest above are my attempt at preserving total credible neutrality, continuing to provide a high degree of ownership guarantee, but at the same time increasing the cost of domain squatting, raising more revenue for the ENS DAO to be able to work on important public goods, and improving the chances that people who do not have the domain they want already will be able to get one.